"Seniors buying Medicare Advantage plans often think — even though they know they’re getting the plan through an insurance company — that they’re somehow still in Medicare or backstopped by Medicare. The reality is they’re neither.

With Medicare Advantage, they’re at the total mercy of the insurance company providing the Advantage plan. They can deny care (and frequently do), refuse to pay for tests, and even refuse to authorize or pay for surgeries and other life-saving procedures. This is their business model, in fact, just like with regular health insurance. The more they can deny care and claims, the more profit they make." - Thomas Hartmann, Stop Medicare Advantage Plans Before Medicare Is Dead

Let's first clear the air here on what Medicare Advantage is. Medicare Advantage (MA) was created by Gee Dumbya Bush and the Republicans with their Medicare Modernization Act of 2003. It basically confected a privatized form of Medicare ("Part C"), with the express purpose of bleeding regular (traditional) Medicare into insolvency by blowing up to $20-25 billion or more a year. (Based on gamed "risk".)

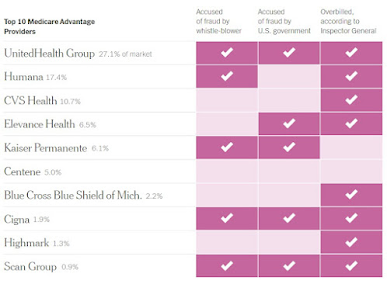

The government pays Medicare Advantage insurers a set amount for each person who enrolls, with higher rates for sicker patients. And the insurers, among the largest and most prosperous American companies have developed elaborate systems to make their patients appear as sick as possible, often without providing additional treatment. See graphic (from NY Times, Oct. 9, 2022):

As a result, a program devised to help lower health care spending (according to the blarney and PR in 2003) has instead become substantially more costly than the traditional government program it was meant to improve. Now the Biden administration has proposed adjustments to halt the bleeding of standard Medicare and the insurers are squealing like stuffed pigs.

The tagline for a new commercial, from the insurance for profit industry ( backed by the "Better Medicare Alliance", is:

“Tell the White House: Don’t cut Medicare Advantage.”

The group has also rallied Medicare Advantage (MA) enrollees to call members of Congress and harass them into dropping the planned adjustment. Which is not a "cut" given the MA plans will still profit, with insurers’ revenue increasing by about 1% on average next year. What exactly, then, is all the caterwauling about? The head of the Medicare agency, Chiquita Brooks-LaSure, said that her agency has “thoughtfully proposed updates that improve payment accuracy” and that Medicare Advantage plans would see an overall increase in payments next year under the proposal.

The proposal by the Centers for Medicare and Medicaid Services would change how the Medicare agency pays insurers. Under a setup called “risk adjustment,” the insurers get more money for enrollees who are sicker, since those patients are likely to need more care and generate higher expenses. The more health conditions that the insurers can document in their customers, the higher their payments from the government are likely to be.

Prior to these proposed changes doctors in the MA system diagnosed illnesses which either: (a) never existed in the first place, or diagnosed conditions that were much worse than they actually were. The effects of either tactic were to amp up the money collected by the MA plans. This despite critics complaining for years that insurers' tactics (a, b above) led to overpayments and more rapid approach of traditional Medicare to insolvency. As the NY Times reported (10/9/22),

"Eight of the 10 biggest Medicare Advantage insurers — representing more than two-thirds of the market — have submitted inflated bills, according to the federal audits. And four of the five largest players — UnitedHealth, Humana, Elevance and Kaiser — have faced federal lawsuits alleging that efforts to overdiagnose their customers crossed the line into fraud."

This is exactly why Medicare itself is heading for insolvency, likely within the next 3 years. The government now spends nearly as much on Medicare Advantage’s 29 million beneficiaries as on the Army and Navy combined. (In 2022, the federal Medicare program spent about $427 billion on Medicare Advantage, according to the Kaiser Family Foundation.)

But the new government proposal would eliminate or trim such overpayments associated with certain marginal conditions that have been hyped by MA plans in the past. (Eg. atherosclerosis, or plaque buildup, in arteries of the extremities, and a specific type of malnutrition.)

In other words, despite all the wailing, weeping and gnashing of teeth by the deficit hawk Reepos, this is a good move. And with some higher taxes on the wealthiest Americans may extend the life of Medicare - the traditional version.

See Also:

by Diane Archer | April 8, 2023 - 6:05am | permalink

Excerpt:

The corporations that run Medicare Advantage plans are engaged in widespread waste, fraud and abuse, resulting in tens of billions of dollars of overpayments to them every year. The advocates and government agencies overseeing Medicare Advantage have spent nearly two decades reporting on this fraud and waste and urging Congress to overhaul the program. Few in Congress or the administration were listening. Now, the Biden administration is finally taking action, but it’s only a first step.

by Wendell Potter | January 15, 2023 - 7:23am | permalink

Excerpt:

Right now, well-funded lobbyists from big health insurance companies are leading a campaign on Capitol Hill to get Members of Congress and Senators of both parties to sign on to a letter designed to put them on the record “expressing strong support” for the scam that is Medicare Advantage.

But here is the truth: Medicare Advantage is neither Medicare nor an advantage.

And I should know. I am a former health-care executive who helped develop PR and marketing schemes to sell these private insurance plans.

And:

Excerpt:

Congress must pass a law to stop the deceptive advertising of Medicare Advantage plans. Only Medicare should be able to call itself Medicare.

Unless you’ve been out of the country for the past few years, you’ve seen the ads on TV featuring Joe Namath, Jimmy Walker, or William Shatner hawking so-called “Medicare Advantage” plans.

Medicare Advantage is not Medicare.

It’s private health insurance being offered to people over 65, with the bill paid for by Medicare. Once you get on an Advantage plan it’s very difficult to get off, and if you’ve been on for more than a year you may not be able to go back to regular Medicare with a Medigap plan at all.

And:

Excerpt:

In my multiple writings on the Medicare Advantage scam, the most common two responses I get (besides, “Thanks, you may have saved my life!”) are, “I’ve never had a problem with my Advantage plan,” and “If it’s so bad, how come so few people are saying so?”

Both are honest, good-faith questions and highlight how easy it is for insurance companies to get away with their Medicare Advantage scams. The answer to both boils down to the unique nature of insurance being the only “product” we buy where we have no idea if it’s any good until something bad happens — which can take years.

Every state in the union has an insurance commissioner. But why?

Why would any state go to the trouble and expense of creating a new layer of bureaucracy?

We don’t have “auto dealership commissioners” or “big-box retailer commissioners”: only insurance has an elected or appointed overseer.

Why would a state want to elect or appoint a very well-paid person to a new position in state government? Why would they appropriate money for a staff, for offices, in some cases even for buildings for a state insurance commissioner?

It turns out the answer is quite simple. One of the easiest scams in the history of scams, going all the way back centuries before Alfred Ponzi set up shop in Pie Alley, is done with insurance.

Here’s how it works.

If you have insurance, you send them a check every month. You think you’re covered and they’ll be there for you when you need them.

But you have no way of knowing if they’ll really be there for you when you need them because you’ve never used the service in a real health crisis.

No comments:

Post a Comment